The Big Tax Regime Question Every Indian Taxpayer Is Asking in 2025

Every salaried professional, business owner, and first-time taxpayer in India is grappling with the same question in FY 2025-26: Should I stay with the old tax regime or switch to the new tax regime — and what happens to my Section 80C investments?

The new tax regime, made the default from FY 2023-24, offers attractively lower slab rates but strips away most popular deductions — including the much-relied-upon Section 80C limit of ₹1.5 lakh. Yet millions of Indians continue to park their money in PPF, ELSS, LIC, and other 80C instruments, half-wondering whether those investments still reduce their tax bill.

The short answer: some do, and some don’t — and the strategy you choose depends entirely on your income level, life stage, and financial goals. In this comprehensive guide, Invancial breaks down exactly which Section 80C investments still deliver tax benefits under the new regime, which ones are worth holding purely for financial returns, and how to stop leaving money on the table every tax season.

What Is Section 80C? A Quick Recap

Section 80C of the Income Tax Act, 1961 allows a deduction of up to ₹1,50,000 per financial year from your gross total income. This single provision has, for decades, been the cornerstone of Indian tax planning. Popular Section 80C instruments include:

- Employee Provident Fund (EPF) — mandatory for most salaried employees

- Public Provident Fund (PPF) — government-backed, 15-year lock-in, EEE status

- Equity Linked Savings Scheme (ELSS) — mutual funds with a 3-year lock-in

- National Pension System (NPS) — long-term retirement savings with an extra benefit under 80CCD

- Life Insurance Premiums (LIC and other insurers)

- Sukanya Samriddhi Yojana (SSY) — for parents of girl children below 10 years

- 5-Year Tax Saver Fixed Deposits — bank and post office

- National Savings Certificate (NSC)

- Home Loan Principal Repayment

- Tuition Fees for up to 2 children

Under the old tax regime, all these investments collectively save you tax by reducing your taxable income. Under the new regime, the rules are different — but not entirely hopeless. Let us explain.

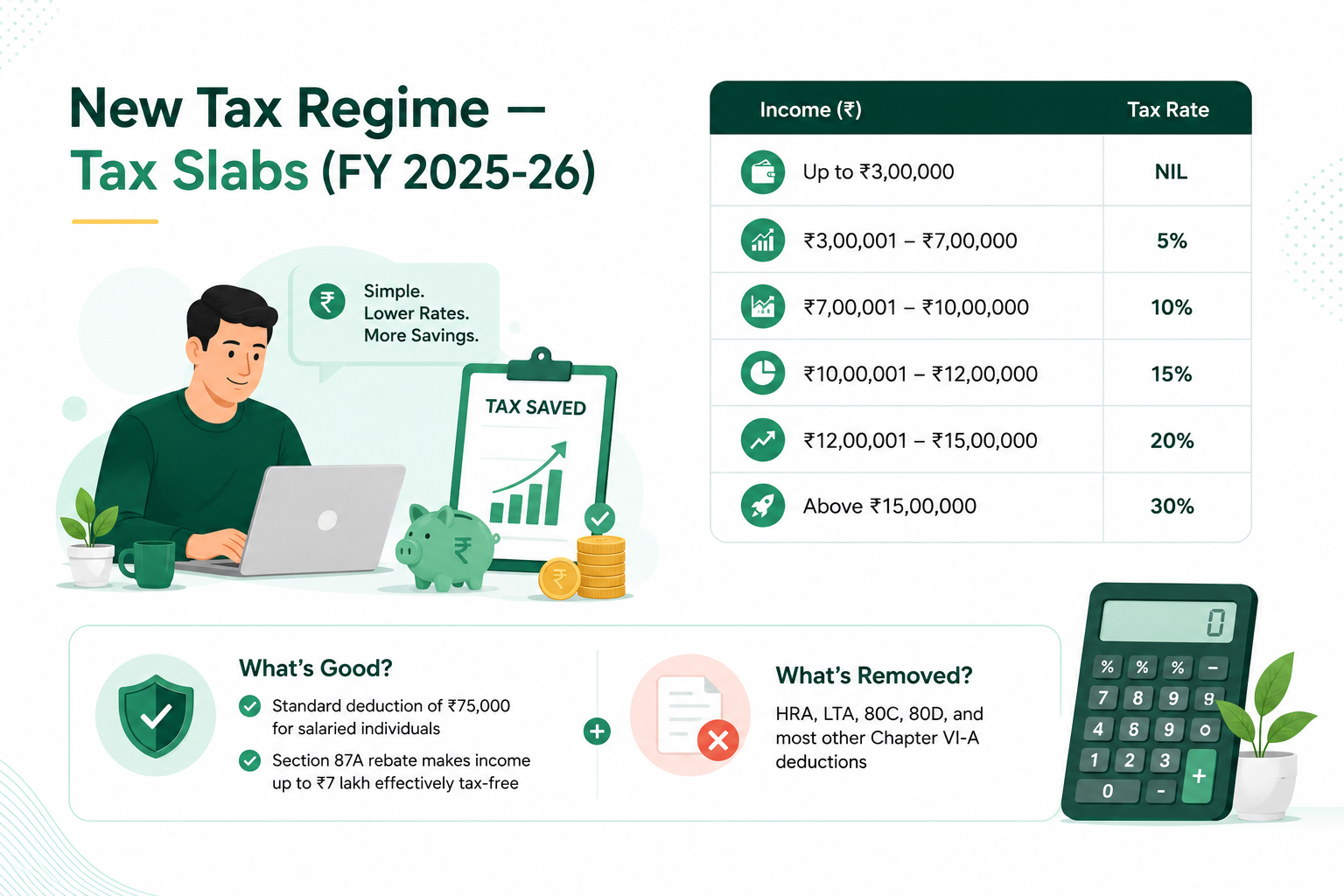

New Tax Regime vs Old Tax Regime: Key Differences for FY 2025-26

Before we discuss 80C, it is important to understand how the two regimes differ at their core. The new tax regime was revamped in the Union Budget 2023 and further refined, making it the default option from FY 2023-24 onwards.

The new regime now offers a standard deduction of ₹75,000 for salaried individuals and a Section 87A rebate that makes income up to ₹7 lakh effectively tax-free. However, it removes HRA, LTA, 80C, 80D, and most other Chapter VI-A deductions.

The old regime retains all these deductions but operates under higher slab rates. For people with significant investments and eligible deductions, the old regime can still save substantially more tax — but the calculation is not always straightforward.

Does Section 80C Work in the New Tax Regime?

This is a hard stop. If you opt for the new tax regime under Section 115BAC, you cannot claim any deduction under Section 80C, 80CCC, or 80CCD(1). The ₹1.5 lakh deduction limit is only applicable if you opt for the old tax regime. However, certain other deductions and tax-free benefits — like employer NPS contributions under Section 80CCD(2) and EEE returns on PPF and SSY — remain available even in the new regime.

However — and this is the part most taxpayers miss — certain tax benefits survive the new regime through entirely different provisions of the Income Tax Act. The underlying investments may also still make excellent financial sense even without the annual tax deduction. Let us look at each instrument in detail.

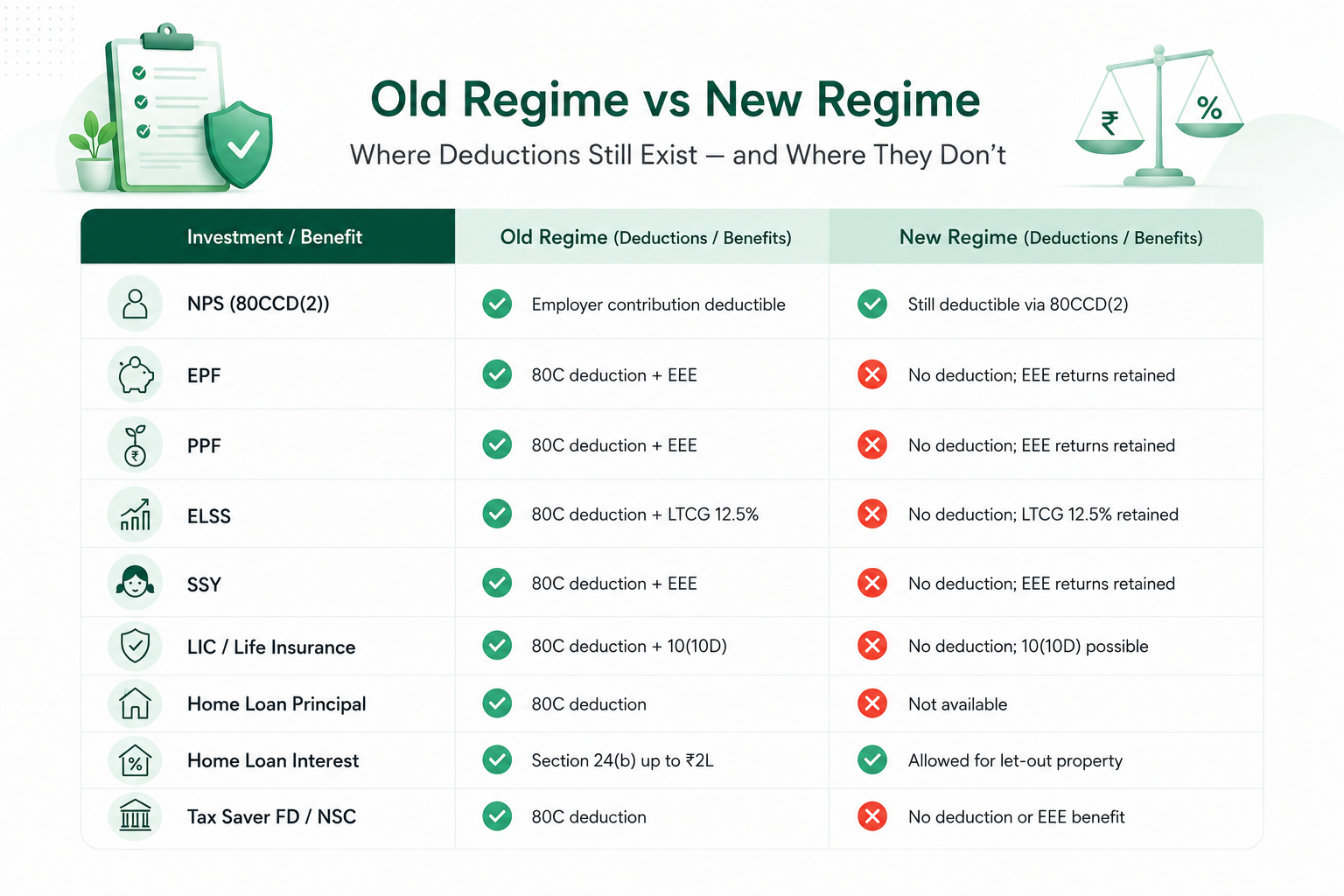

Section 80C Investments That STILL Save Tax in the New Regime

1. NPS (National Pension System) — Section 80CCD(2): The Star of the New Regime

NPS is the single most powerful tax-saving tool available under the new tax regime. Under Section 80CCD(2), employer contributions to your NPS Tier-I account are fully deductible — even under the new regime. Here is how it works:

- Government employees: Employer NPS contribution up to 14% of Basic + DA is tax-free

- Private sector employees: Employer NPS contribution up to 10% of Basic + DA is tax-free

- This deduction is over and above the standard deduction of ₹75,000

- Depending on salary structure, this can mean ₹30,000 to ₹1,00,000+ in additional tax savings

2. EPF — Tax-Efficient Accumulation Without the Annual Deduction

EPF contributions by employees do not qualify for a deduction in the new regime. However, the EPF continues to be a highly tax-efficient instrument in the accumulation and withdrawal phase:

- Interest earned on EPF contributions up to ₹2.5 lakh per year remains completely tax-free

- The final withdrawal amount after 5 years of continuous service is fully exempt from tax

- EPF thus acts as a tax-efficient, government-backed wealth-building instrument — just not as an annual deduction tool under the new regime

3. ELSS Funds — Tax on Exit, Not Entry, and Still the Best Equity Option

ELSS no longer gives you an 80C deduction in the new regime. However, Equity Linked Savings Schemes remain among the best equity mutual fund instruments available to Indian investors:

- 3-year lock-in enforces investment discipline, shorter than PPF or NPS

- Long-Term Capital Gains (LTCG) tax on ELSS redemption is 12.5% on gains above ₹1.25 lakh — applicable in both tax regimes

- Historically, ELSS funds have delivered 12–15% CAGR over 10-year periods, outpacing most fixed-income instruments

- The tax saving on entry may be gone under the new regime, but the wealth creation potential remains unmatched among all 80C instruments

4. PPF — The EEE Champion That Still Makes Sense

PPF contributions do not earn you an 80C deduction in the new regime. However, PPF retains its Exempt-Exempt-Exempt (EEE) tax status — which means:

- The interest earned on PPF is completely tax-free every year

- The maturity amount after 15 years is fully exempt from income tax

- The current PPF interest rate of 7.1% p.a. (compounded annually) is effectively much higher on a post-tax basis compared to a taxable FD

- For conservative investors building a long-term retirement or child education corpus, PPF remains one of the most tax-efficient products in India

5. Sukanya Samriddhi Yojana (SSY) — EEE Status Fully Retained

Like PPF, SSY continues to enjoy EEE tax treatment under both tax regimes. Contributions no longer give you the 80C deduction in the new regime, but the account’s interest and maturity amount remain fully exempt from tax. The current interest rate of 8.2% p.a. makes SSY one of the highest-returning government-guaranteed EEE instruments available. Parents of girl children should continue SSY as a non-negotiable long-term financial planning tool regardless of which tax regime they choose.

6. Home Loan — Interest Deduction on Let-Out Property Survives

Home loan principal repayment under 80C is not available in the new regime. However, the interest deduction under Section 24(b) is available for let-out property even in the new tax regime — meaning home loans still carry indirect tax efficiency alongside the powerful asset creation benefit. If you own a rented-out property and have a home loan, your net annual value income can be reduced by the full interest paid.

7. Life Insurance — Tax-Free Maturity Under Section 10(10D)

LIC and ULIP premiums do not get an 80C deduction in the new regime. But life insurance policies can still deliver tax-free returns at maturity under a separate provision:

- Section 10(10D) exemption applies if the annual premium is less than 10% of the sum assured

- For ULIPs issued after February 2021 with annual premium above ₹2.5 lakh, LTCG tax applies on gains

- Always verify the 10% premium-to-sum-assured ratio when purchasing a new policy to preserve the maturity tax exemption

Side-by-Side Comparison: 80C Instruments in Old vs New Regime

How to Choose: Old Regime vs New Regime — A Decision Framework

The decision between old and new tax regimes should always be based on cold numbers, not habit or inertia. Here is a practical framework:

Choose the Old Tax Regime if:

- Your 80C investments total ₹1.5 lakh per year

- You pay HRA and can claim a substantial HRA exemption

- You have home loan interest above ₹2 lakh under Section 24(b) on a self-occupied property

- You pay health insurance premiums eligible under Section 80D

- Your income is above ₹15 lakh and your total deductions are substantial

- Your total deductions (80C + 80D + HRA + home loan interest) exceed ₹3.75 lakh

Choose the New Tax Regime if:

- You have minimal deductions or investments

- Your income is between ₹7 lakh and ₹12 lakh and you lack significant deductions

- You prefer simplicity and a lower compliance burden

- Your employer already contributes to NPS under Section 80CCD(2)

- You are a freelancer or business owner with limited eligible deductions

- You are young, just starting out, and haven’t yet built a large deduction portfolio

Smart Tax Planning Tips for FY 2025-26

- Calculate your tax liability under both regimes before the start of the financial year — not in a March rush

- Maximise employer NPS contribution restructuring under 80CCD(2) regardless of which regime you choose — this is regime-neutral tax saving

- Do not invest in 80C instruments solely for tax saving if you have chosen the new regime — evaluate each product on its financial merit

- Use ELSS for long-term equity wealth creation — it remains the only 80C-linked product that directly invests in equity markets with a short lock-in

- Continue PPF and SSY for their EEE tax efficiency on returns — the compounding effect over 15+ years is enormous

- Inform your employer of your regime preference at the start of the financial year to ensure correct TDS deduction throughout the year

- For business owners: switching back from the new regime to the old regime is allowed only once in a lifetime — decide carefully

- Review your CTC structure annually with a tax advisor — your financial situation changes every year

- File your ITR before the July 31 deadline to avoid late fees and preserve refund priority

Let Invancial Help You Save More Tax: Not sure which tax regime is right for you in FY 2025-26? Our certified tax advisors at Invancial will analyse your income, investments, and financial goals to build a personalised tax-saving strategy — so you never pay more tax than you need to. Book your FREE Tax Planning Consultation today.